Adapting to Change: An Investor's Guide to Office Building Redevelopment

The office real estate market has been significantly impacted by distress and transformation in recent years. Changing cultural preferences, rising interest rates, and market dislocations have propelled the office sector into uncharted territory. While the COVID-19 pandemic was a significant driving factor, it was far from the only one. Office vacancies are at a 30-year high, as changes in how people work have placed newer and smaller office spaces in higher demand. Declining Class A office rents have indirectly impacted Class B and C rents by creating competition to retain tenants, as there’s been a shifting tide to “cheaper” and newer office space. Alongside higher interest rates, elevated vacancy risks, and lenders' hesitancy to extend debt on office buildings, office cap rates have widened, thus bringing down office values. With these factors in play, the market has shifted toward all-cash or very low leverage transactions, and brokers and investors have made a strategic shift to evaluating the underlying land value for potential redevelopment, due to the suppressed and dislocated office investment sales values. So, how does an investor come out ahead despite all these challenges? Read on for the answers.

Market Dynamics and Opportunities

Vacancies are at the heart of office market challenges, as operators have struggled to retain and bring in new tenants. The once-beloved office footprint of '70s–'90s vintage has struggled to stay competitive; couple this with widening cap rates and elevated interest rates, lenders see office building debt as high-risk, and all-cash transactions are commonplace.

As office values have declined, it’s created a pivotal moment for astute investors and developers, as they evaluate the underlying land value and look for the best property uses over the long term. If this is done properly, it is possible to do more than simply weather the current upheaval. There is latent potential in the evolving office landscapes, but a keen and studied eye will be required to discern the true opportunities from the potential money pits.

Identifying Redevelopment Prospects

Identifying redevelopment prospects starts with defining the criteria to be used. Both the criteria and how they are weighted can vary based on the specific property. The vintage of the office property plays a crucial role in identifying potential added costs, such as asbestos remediation, and in the case of adaptive reuse, structural integrity and adaptability. Parking, both current and potential, will impact future uses significantly. Occupancy rates will identify underutilized properties, with anything under 70% considered to be low. Investors/developers also want to look at the existing leases, with the ideal range being under three years. And, of course, the surrounding area and factors such as the local job market, walkability, and neighborhood demand drivers will determine whether a planned project will even have the ability to attract residential tenants.

At the same time, redevelopment is never a one-size-fits-all situation. Single-phase projects offer simplicity and a focused approach, suitable for redevelopment of existing individual office buildings. Mixed-use multiphase redevelopment projects of large office parks or developments combining residential, hospitality, and commercial elements offer a greater potential reward in exchange for a more complicated execution. Deciding on the right redevelopment approach takes more than just looking for demand in the market. Investors need to understand the property and whether it suits their intended project. In addition, large scale mixed-use redevelopment demands a much more complicated capital execution which frequently involves a lot of structure around the capital stack.

To Rebuild or Not to Rebuild

Investors in this market must strategically evaluate the underlying land value, as well as the best long-term uses with the highest returns. This means looking at the potential for redevelopment, conversion, and adaptive reuse, all of which require meticulous analysis of criteria such as vintage, parking space (including repurposing existing parking structures), occupancy levels, lease terms, and the vibrancy of high-growth markets. When looking at tearing down and rebuilding, such as when redeveloping from office to multifamily housing, the floor area ratio (FAR) multiple helps investors determine feasibility and align investment with land redevelopment value. FAR makes it possible to estimate the potential square footage of future development based on the existing square footage. In our experience, the minimum multiple of current to projected FAR is 3:1 in order for land value to exceed the current use, all things considered.

Overcoming Challenges in Office Redevelopment

Identifying suitable office properties for redevelopment requires a nuanced understanding of many complicated factors. Properties need to align with the vision of redevelopment and not present significant obstacles that could derail the project or create excessive timelines. Ensuring a positive outcome, therefore, requires meticulous planning and a strategic approach which includes entitlements, existing lease timelines, reciprocal easement agreements (REAs), utility capacity, capital structures, and sometimes multiple product development expertise to name a few.

Navigating political obstacles, zoning restrictions, and even local special interest groups is essential to the planning process. Developers should try to understand the larger landscape they are stepping into before delving too deep into a project. From adeptly navigating bureaucratic landscapes to handling local cultural sensitivities, redevelopment requires more than just understanding the property itself. Developers also have to look into all applicable REAs, easements, building code requirements, and rezoning sensitivities and timelines. Most property owners are purely operators and possess little of the required information that developers require, so careful research is necessary.

At the same time, developers will have to navigate capital market challenges which can best be described as currently finicky as both debt and equity remain squeamish amid high-rate environments and overbuilding in many markets. In addition, construction costs have increased significantly over the past decade, and developers may have to recalibrate and recalculate even while construction is underway, which means accounting for large contingencies in their development models. With so many potential complications, developers need to be well-versed in a myriad of factors that impact their developments.

The Impact of Interest Rates on Redevelopment

The relationship between rising interest rates and increased cap rates informs a nuanced understanding of the redevelopment landscape. Rising interest rates in recent years have pushed cap rates higher. As the cost of borrowing goes up, the cap rates have to be raised to compensate for the added cost to projects. Investment becomes more expensive, and funding is also more difficult and expensive for investors to acquire. The unpredictability of the market leads developers to widen the cap rate and yield on cost (YOC) gap to maintain profitability, which sends a ripple effect through the market.

The resulting landscape is notably more intricate, demanding a strategic understanding of how interest rate fluctuations impact redevelopment feasibility and profitability. The challenges in capitalizing deals under current assumptions come to the forefront as interest rates and cap rates rise. Everyone involved in redevelopment must find new strategies, including developers, who must solve a widening gap between exit cap assumptions and YOC. Construction debt has also become both more costly and anemic, with lower loan-to-cost (LTC) ratios requiring increased equity to even get a project funded. In addition, many lenders require on hand deposits in the 10%-20% range to fund their loans. This can be a checkpoint for determining the viability of a redevelopment project, and redevelopment deals need to be judiciously structured to ensure success.

Identifying Funding Sources for Redevelopment Deals

As development funding sources get squeezed, it's important to look at all possible options. Luckily, there are plenty. Many local and regional players, such as regional and national multifamily developers, are funding projects when there is a clear path on entitlements and vacating the existing buildings. Family offices and developers with office exposure who have the capacity to manage existing office properties while working through entitlements and predevelopment work are also able to be a little more flexible with specific scenarios that might drive others away. Often times well capitalized investors seeking to maintain their equity positions are willing to joint venture their office buildings with multifamily developers in a land contribution to Limited Partner or Co-General Partner position.

Of course, developers can also take advantage of tax incentives to make up for some of the increased development costs. This usually still assumes that a developer will have the money to cover costs upfront and reap the advantages later. However, that dynamic can change if the incentive is on the investment. One example of this is Opportunity Zones, which are areas that have been designated as desirable for redevelopment. Opportunity Zone Funds are investor vehicles that specifically invest in such areas to reap tax benefits and can serve as a funding source for developers.

Similarly, Real Estate Investment Trusts (REITs) can play a key role. Whether private or public, REITs bring a wealth of experience and financial clout to the table. At the same time, the increasing size and sophistication of REITs make them well-suited for large-scale redevelopment projects, and they may partner with developers. REITs may also directly acquire and redevelop properties. Many large REITs not only have significant development experience but can fund developments on balance sheets eliminating the need for outside debt and equity capital.

Redevelopment as a Solution to Housing Shortages

The U.S. has an acute housing shortage, with some areas struggling more than others. Redevelopment stands out as a promising solution to this crisis. This is particularly true for the office real estate market, where the recent depreciation in values make properties all the more attractive for multifamily redevelopment. With high vacancies and a shift in cultural preferences toward work from home and to newer, smaller-footprint office spaces, many traditional large office buildings are simply no longer competitive. This type of redevelopment can also meet the desire for residential space with proximity to work and urban amenities.

At the same time, redevelopment does not have to completely transform land use. Mixed-use developments and even hotels can offer an alternative approach that maximizes the potential of the property. This type of strategic diversification also enables development projects to align with the unique demands and characteristics of an area.

The availability of government incentives can also influence redevelopment choices. These include federal initiatives such as the Housing Supply and Action Plan and the Community Development Block Grant, which are often designed to encourage redevelopment or development of an area and spur economic growth by encouraging private investment. Such programs provide financial support and incentives for developers and investors transforming commercial spaces into residential units.

Sustainability and Redevelopment

Sustainability and redevelopment can form a symbiotic relationship that extends beyond meeting regulatory requirements. Redevelopment can actively engage with and enhance sustainability goals, contributing to creating vibrant, eco-friendly urban environments.

Almost every jurisdiction in the U.S. has integrated sustainability principles into building codes, setting the stage for a more environmentally conscious approach to development. These codes shape the redevelopment landscape, and compliance ensures that new projects are going to be more sustainable than those built in the past. Older buildings, such as existing office structures, are much less likely to meet these more modern requirements. Tearing them down and redeveloping them as multifamily housing can, by its very nature, greatly improve the sustainability of the area.

By conforming to building codes that prioritize sustainability, redevelopment projects actively reduce their ecological footprint compared to existing structures. While tearing down and building new may not seem intuitive, it makes a lot of sense when compared to either leaving older buildings to consume more energy and resources or attempting to rehab an older building under strict constraints.

Navigating the Supply Surge in Multifamily Development

The multifamily development sector is currently in over supply, but the astute investor's focus should not be solely on the volume of units. The better approach for both investors and developers comes with strategic positioning in areas where long-term demand-supply metrics presents the best opportunities for success.

The recent increase in multifamily development supply is a direct response to the evolving dynamics, low vacancies, changing preferences post-COVID-19, and appetite for multifamily development by debt and equity providers. While demand for office investments wains, investors understand the long-term benefits of multifamily developments, and even now that fundamentals have temporarily eroded, the U.S. remains under-supplied in housing.

Given the dearth of recent housing starts as we enter our sixth quarter of high interest rates, an inevitable supply gap is forming. New starts in multifamily development are already anemic, and demand for new housing units might outpace the actual construction as early as mid-2025 in some markets. By strategically identifying and acquiring development sites with the potential to bridge the anticipated supply gap, investors and developers can be poised to take advantage when the time comes.

A data-driven approach is the key to finding the right property for redevelopment. We recommend looking at the new jobs-to-absorption ratio in a market to help evaluate the need for additional housing. As an example, the long-term job-to-absorption ratio for Austin, Texas is four jobs to one new unit absorbed. With that information, an investor or developer can then look at the projected employment growth in an area and the number of new starts in the previous year to project when the optimal time to begin new construction will occur.

All in all, while it’s heavily nuanced, office conversions and redevelopments serve as a meaningful alternative to office owners that are struggling by shifting the near-term focus to evaluating the highest and best use for the asset and underlying land.

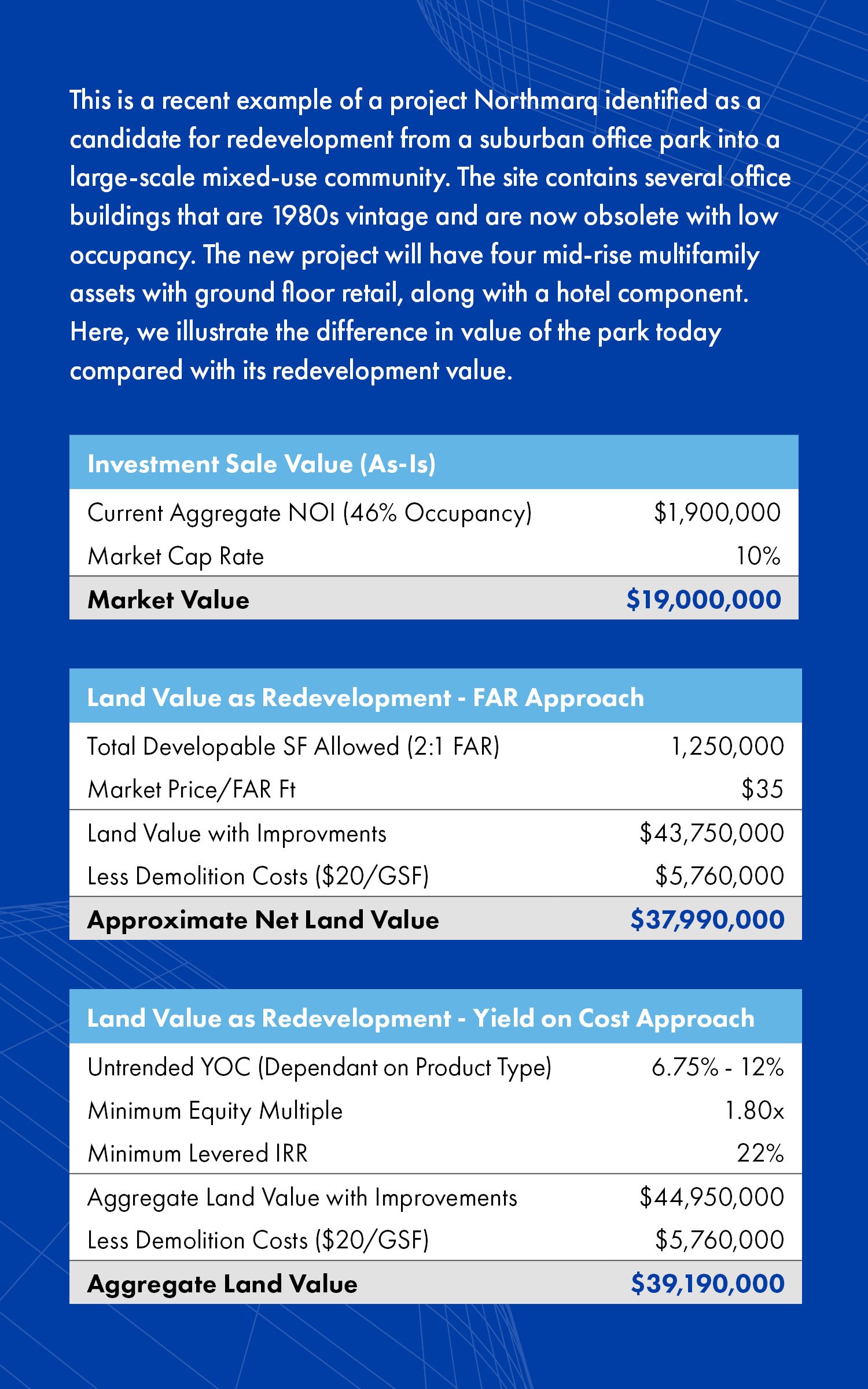

With vast redevelopment experience, Northmarq’s National Development Services team currently has in excess of three million square feet of office and commercial redevelopment opportunities in the market today. Each of these projects provide the ability for building owners to garner a significant premium to their current investment sales value.

Insights

Research to help you make knowledgeable investment decisions